Creator Capital: A Proven Framework For Taking Control Of Your Career, Money, And Financial Freedom

Agency isn’t something you’re handed — it’s something you design.

Arrrrr! 🏴☠️ Welcome to a 🔒 subscriber-only edition 🔒 of Category Pirates. Each week, we share radically different ideas to help you design new and different categories. For more: Dive into an audiobook | Listen to a category design jam session | Enroll in the free Strategy Sprint email course

Dear Friend, Subscriber, and Category Pirate,

Agency is a word that hits different, depending on where you are in life.

For a recent college grad, agency might mean having the freedom to take a job that excites you — not just one that pays the bills.

For a young parent, agency might mean having time to build a business while raising kids.

For someone in the second half of their career, agency might mean cutting back on your hours to travel, spend time with friends and family, or explore your treasure-hunting hobby. (ARRRR!)

At its core, agency means freedom.

The freedom to make your own choices — to act independently and shape your life on your terms. It’s the power to say, “I’m doing this.” And actually doing it.

You do what you want. With who you want. When you want.

Not because someone gave you permission, but because you claimed it.

As Perplexity puts it:

“Having agency means possessing the capacity to act independently and make choices that influence one's life and environment.

It refers to an individual's sense of control over their thoughts, behaviors, and circumstances. Agency empowers a person to initiate actions, set goals, and work towards achieving them, rather than merely reacting to external forces.”

If you’re starting your career or scraping by, you might think this sounds like hopeful, happy horseshit. Because you’re sweating the rent, living paycheck to paycheck, or stuck in a grind that drains your soul. For too many people, agency feels like something reserved for the lucky.

The truth is…

Agency isn’t something you’re handed. It’s something you design.

Take Pirate Katrina. At 23 years old, she decided to leave a good copywriting job at an ed-tech startup to go out on her own as a freelance writer. She turned down a potential job at Google — a decision that meant walking away from an estimated half a million dollars in equity — because agency mattered more.

Almost ten years later, Pirate Katrina has lived in over 24 Airbnbs in dozens of cities and countries. Having agency to travel the world while working remotely on projects she cared about led to:

Spending three years in Switzerland, chasing mountain adventures and helping scale a ghostwriting agency to $2+ million in revenue.

Running the editorial team at a high-growth finance start-up while living out of a van in places like Phoenix, Joshua Tree, Seattle, Golden, Vancouver, and Banff

Fulfilling a lifelong dream of learning to paraglide while growing Category Pirates and helping 50+ entrepreneurs define their category in the Category Design Academy

She did all of this while building a career and life she loves.

(Which she thinks is worth at least $500,000.) 🤑

Agency isn’t a given.

It’s a choice.

🔊 Want to listen to this mini-book instead? Head to the audiobook.

Radical personal agency is built on (your relationship) with money.

Note: We purposely did not say, “Radical personal agency is built on money.” We did say, “Radical personal agency is built on (your relationship) with money.”

More on that soon.

This is important because 63 percent of American adults report money as a top stressor, and 65 percent say work is a significant stressor in their lives.

A healthy relationship with money, plus a well-designed financial runway, lets you stop reacting to the world and start creating your own (different) future. And it’s how you turn agency from an abstract idea into your life.

Agency gives you:

The freedom to say no. You’re no longer shackled to toxic people, soul-sucking jobs, or projects that don’t align with your values. when someone offers you a deal that compromises your integrity or drains your energy, you can walk without worry.

Time to focus on what matters. You gain the luxury of prioritizing long-term goals over survival. whether it’s starting your dream business, mastering a new skill, or spending quality time with your family, you have the bandwidth to invest in what truly matters to you.

The power to take risks. Financial stability lets you make (more) bold moves, like launching a business, moving to a new city, or pivoting to a different industry. Risks aren’t as scary when you build your own safety net.

Ability to invest in yourself. You can afford to spend money on learning, growth, health, and opportunities of your making. A powerful relationship with money (coupled with a well-designed financial runway) gives you the means to level up, whether you take a course, hire a coach, travel to gain new perspectives, or improve your health.

Peace of mind. Agency and a solid financial runway reduce anxiety and stress. Instead of being in survival mode, you’re free to think creatively, solve problems effectively, and pursue joy.

In Silicon Valley and on Wall Street, this is called ‘F.U. money.’ The thinking goes: If you have enough money, you can tell people to F-off.

We prefer to call it “Free You money.” ARRRR!

Building your financial runway doesn’t mean you’ve reached every destination. It means you’re equipped to chart your course (whatever that may be) with confidence, clarity, and choice.

That’s the essence of agency.

If you’re in a tough spot right now. Please. Know. We don’t just empathize — we’ve been there, and we feel you. While we don’t know exactly what you're dealing with, we are not children of wealth or entitlement. We’ve lived through some of the hardest, messiest, most gut-wrenching, poop-your-pants-scared moments in life and business. (More than once.) And while we’ve been blessed with loving family and friends, the three of us didn’t start with much of anything. And we’ve had to walk through serious fire in life. While we can’t know exactly what you’re dealing with, we feel you.

When you have nothing, dream a big dream.

Dreams of a different future are the raw materials of constructing your legendary life.

The legendary Stephen Covey wisely taught us to “begin with the end in mind.” This thinking shifts your focus FROM where you are now, TO where you could be. (What in category design is called a FROTO.) And it gives you a sense of control over your life.

Humans thrive when they have control (a say) in what to make of their lives.

That’s because Control = Freedom. When we take control of our lives (and circumstances), we increase our personal freedom. You could argue that freedom is the ability to control your destiny. (Design a different future.) This applies to every dimension: work, family, friends, community, faith, sports, and activities. And by “control,” we don’t mean wack-a-do, overbearing, micromanaging, obsessive behavior. We’re talking about personal agency. Your power, control, freedom, and authority over your own life, actions, and surroundings.

Pirate Al Ramadan (co-author of Play Bigger with Pirate Christopher) explains to young people that what financial success really does is create more choices in life.

Now, let’s zoom in on what that means.

Does Your Money Own You, Or Do You Own Your Money?

There are two things about money to consider when building agency:

The money itself

Your relationship with money

We’ve met ski boot fitters who couch surf and live out of old vans, yet have radical agency and the happiness that comes from living life on their terms. And we’ve met miserable billionaires whose money owns them. Pirate Eddie worked with a billionaire who refused to fly to the US out of tax fears. Pirate Christopher knows a billionaire who got divorced because he and his wife fought non-stop about…wait for it…

Money.

What good is having all the money in the world, if your money owns you?

The same is true for people who are owned by not having money.

Pirate Christopher recently had a conversation with a smart, capable 56-year-old guy who made slightly above the poverty line last year. He explained the problem — his small business employer was run by morons. When asked about his prior jobs, he said he had to leave those companies because they too were run by morons. When asked about any new job prospects, his response: “No one in this town knows how to run a business.”

Not having money can own you.

(It used to own us.)

Struggling can be part of our identity. We’re lured into thinking we are a person with little money. Becoming financially successful would require a new self design. Being rich, would nullify our self narrative. And it’s hard for most people (like us) to accept a new identity design.

Most people say things like, “That’s just how I am.”

As if they had no choice in being the person they are. As if they had no ability to change or grow. Or no way to create a new (different) way for their life?

Having money or not having money — can own you.

Here’s some mental scaffolding for how to own your money:

When your life is about money, your life is about money.

When your life is about living (and money is simply the tool to fuel it), you can have radical agency.

Taking personal responsibility for one's life and circumstances is the only way to be successful. If you own your life situation, you can fix it. If you’re responsible, you are the designer, author, and creator of your life. And your money.

Let that cook in your cranium.

Now, let’s unpack one of the big barriers (some) people face in their relationship to money.

Breaking the “Money = Bad” Narrative

“If you make money, you must be mean, horrible, or crooked.” Many of us grew up surrounded by this kind of thinking. We get it.

But here’s a truth: The saying “money is the root of all evil” is a misquote from the bible.

Read that sentence again. ☝️

The good book actually says, “The love of money is the root of all kinds of evil.” The bible does not say being wealthy is necessarily good or bad. For example, Job (a very good and prosperous family man from the bible) had livestock and land assets worth about $250 million in today’s dollars — and he was celebrated as blameless and upright.

Character and cash flow are not necessarily correlated.

Money is not the problem. The issue is character, choices, and what you want to create.

“Money does not change you; it magnifies what you already are.”

When someone says, “If you’re rich, you must be a bad person,” recognize it for what it is: a self-soothing excuse. This bullshit is fed to us by people who are not financially successful, trying to make themselves feel better. You see, if “only assholes get rich” you have a great (pre-built) excuse for failing. If you accept this broken mental scaffolding, you not only set yourself up for failure — you guarantee it.

Legendary people don’t buy this. Legendary people don’t trade in excuses.

Making our favorite calculus:

Results ≠ No Results + An Excuse.

Take Jim Carrey, for example. Long before he was a Hollywood superstar, Carrey was a struggling actor, living in poverty and dreaming of success. He refused to let his circumstances or the belief that money was "out of reach" hold him back.

In 1985, Carrey wrote himself a check for $10 million, dated Thanksgiving 1995, with the memo: “for acting services rendered.”

He carried that check everywhere, using it as a powerful visualization.

Often, he’d drive to the top of a hill in Los Angeles, sit in his beat-up Toyota, and imagine himself as a successful actor, celebrated by directors and admired by peers. Carrey’s approach wasn’t magic. It wasn’t about writing a check and waiting for the universe to deliver. As he famously said, “You can't just visualize and then, you know, go eat a sandwich.” Visualization was a way to make himself believe that success was possible — that it was already out there, even if he hadn’t achieved it yet.

Just before Thanksgiving 1995, Carrey was cast in Dumb and Dumber — for 10 million dollars.

Carrey’s story isn’t about manifestation.

(Make no mistake. We’re not in the visualize it, sit around drinking beer, and let the law of attraction work for you, whoo-hoo, blah-blah, ding-dong cult.)

It’s about the power of a mindset that refuses to let external circumstances define what’s possible. It’s about recognizing that money — when paired with hard work and a clear vision — can be a tool to design your life.

Money is not something to fear or avoid. It’s the fuel for your dreams.

So, the next time you catch yourself thinking, “money is bad” or “rich people are greedy,” remember Jim Carrey’s check in his wallet. It wasn’t the check itself that changed his life. It was the mindset it inspired and the hard work that followed.

This brings us to an important a-ha:

Your relationship with money shapes your entire approach to life.

(A zebra hole: When Pirate Christopher was in his early 20s, he ended up at a CRM conference dinner in Boston with some super-ding-dong software entrepreneurs. Over drinks, a young reporter asked a founder why he retired young after selling his company. “I made enough. And now, I want to do something different,” he said. We’re wired for more. Which makes “enough” an interesting thing to think about.)

The more money you make, the bigger difference you can make for yourself, your family, and your community — no matter how big or small your world is.

That’s where building a financial runway comes in.

The 2 Ways To Build Your Financial Runway

Your relationship with money determines your trajectory, and your financial runway is the on-ramp to your dreams.

And while the ultimate goal is to create a life where your investments “pay for the party,” there are two primary ways to build your financial runway to get there. These two approaches aren’t mutually exclusive. In fact, they often overlap. But understanding them can help you design your runway.

Option 1: Sell your time for money.

We all start out the same way, selling our time for money.

It’s where most careers begin — and that’s okay. Good, even. After one of Pirate Christopher’s nephews got his first job at a mini-golf course, Christopher asked him what he was learning. “Getting paid almost nothing to do this mindless job is no fun,” the nephew responded.

The sooner you learn that selling time for money is a treadmill, the better. Every dollar earned this way requires your active effort. And the moment you stop working, the money stops, too.

Even worse, there are only 24 hours a day you can sell. So consider this:

No one gets rich selling their time for money.

No one gets rich selling their time for money.

No one gets rich selling their time for money.

No one gets rich selling their time for money.

No one gets rich selling their time for money.

No one.

Your mission is to shift from working for money to making money work for you.

Once your investments “pay for the party” (cover your after-tax living expenses), you are free.

Imagine you’re on the couch, sipping your favorite drink, bingeing 70s sitcoms, and every single one of your living expenses is covered. Not because you’re working. Not because you’re hustling. But because you’ve built a financial runway that takes care of everything without requiring your time.

Funny story:

Pirate Christopher witnessed this firsthand as the CMO of Mercury Interactive, an enterprise software company. After acquiring a startup, some founders stayed on, some left, and others were shown the door. One founder (we’ll call him Jimmy) was in the latter category. At Jimmy’s going-away party, Christopher asked him, “So, Jimmy, what are you going to do now?”

Jimmy, in his 40s, looked Christopher straight in the eye and said, “Watch TV.”

That’s it. That was the guy’s plan for many years to come.

Jimmy had made enough money to stop selling his time for money. So he could sit on the sofa and watch tv all day, every day, for the rest of his life. But most people want (and need) more purpose than that.

Jimmy’s story is a reminder of the power of a financial runway.

It’s not just about freedom from work — it’s about freedom to design your life on your terms.

P. S. - After a decade of TV watching, Jimmy couldn’t take it any more. So he started a company, proving (yet again) that work provides meaning, not just income. Work is how we create and contribute value. And human beings must feel valued to be happy.

Option 2: Build your Creator Capital.

Radical agency — the kind that lets you live on your terms — takes more than financial stability. (If it were that simple, anyone with basic financial knowledge and spreadsheet skills could design their dream life.)

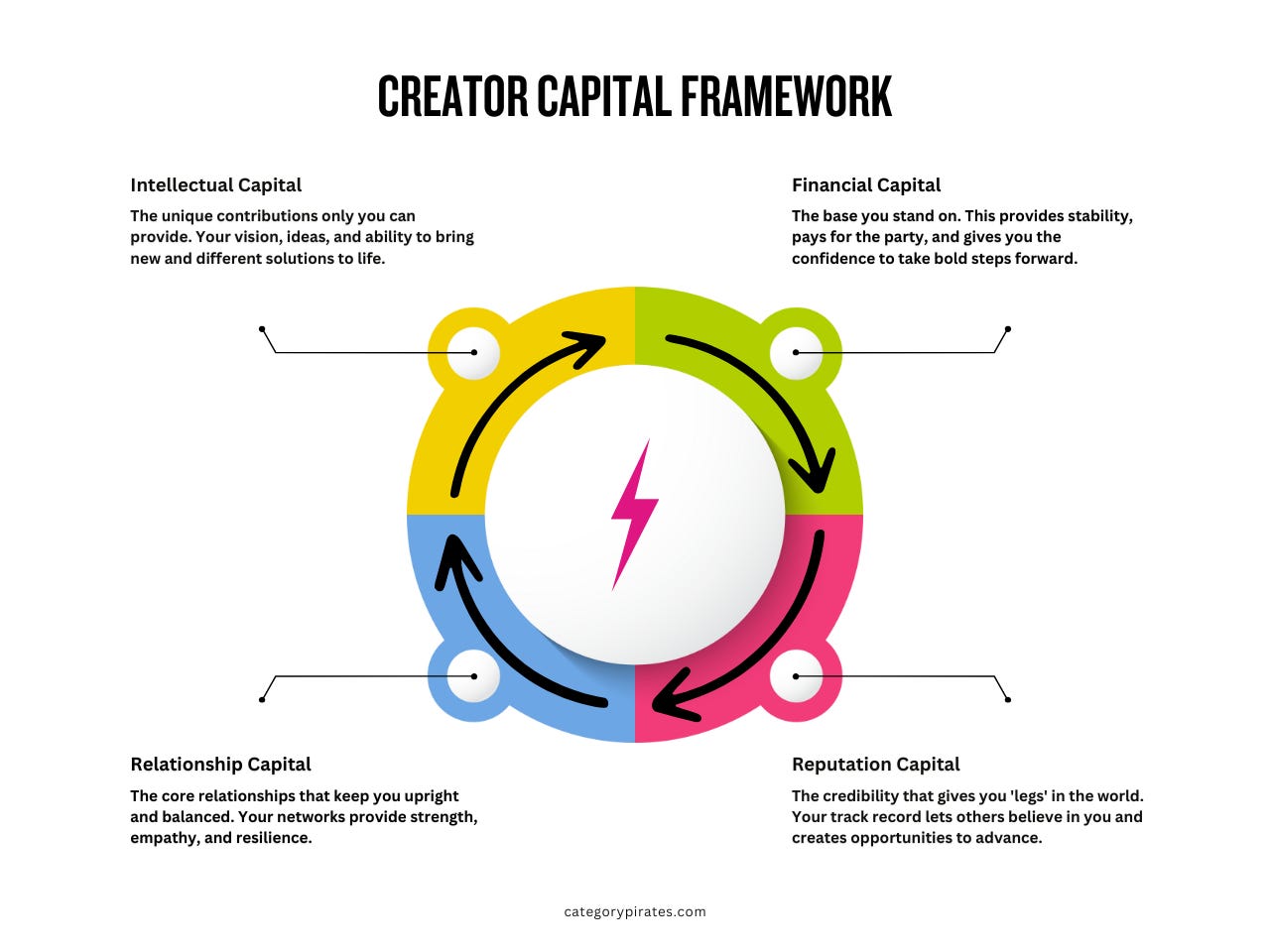

The most powerful way to build your financial runway and unlock agency is by turning your earnings into four types of Creator Capital that work for you.

Financial Capital gives you the resources to take risks and invest in yourself.

Reputation Capital opens doors and brings opportunities to your doorstep.

Relationship Capital connects you to the people who will elevate and sustain you.

Intellectual Capital allows you to scale your expertise and impact.

These aren’t just passive investments. They’re dynamic assets that work together to amplify your ability to create, grow, and sustain wealth. And just as important, they help you build a life of meaning, freedom, and resilience. It’s about having a foundation where each form of capital fuels the others. Because when you grow all four capitals together, you create a flywheel effect that amplifies your ability to design a life that aligns with your values and aspirations.

Let’s dive into how this works.

The Creator Capitalist Framework

The Creator Capital framework is designed around four pillars that hold up your financial runway and, ultimately, your career.

Financial Capital is your savings, investments, and systems for generating passive income that pays for the party.

Reputation Capital is what you’re known for that brings opportunities to your door—it’s built on trust and driving extraordinary outcomes for others.

Relationship Capital is your network of people who vouch for you, amplify your efforts, sustain you through challenges, and support your wins.

Intellectual Capital is your intellectual property, products, content, or services that scale beyond your time and let you earn without trading time for money.

Each of these Creator Capitals is vital in designing your carer and financial runway. Financial Capital pays for the party. Reputation Capital brings opportunities to your door. Relationship Capital lifts you up, keeps you going, and helps you stay grounded. And Intellectual Capital allows you to earn without trading time for money.

(And in case you’re wondering, your superpower is the connective tissue.)

Before you can design a runway that gives you radical agency, you have to understand how these Creator Capitals work together. They’re not separate — they’re interconnected. Each one amplifies the others.

For the rest of this mini-book, we’ll dive deep into Financial Capital.

(Don’t worry, we’ll cover the other ones in upcoming mini-books!)

Financial Capital is how you “pay for the party.”

Financial Capital is the foundation of your financial runway.

This is the money you’ve saved, invested, or earned that lets you cover your expenses and fund your ambitions. It allows you to transition from trading time for money to building freedom. It’s not just about having money. It’s about having enough money to sustain your life and fuel your ambitions.

Financial Capital matters because:

Without it, you’re tied to the grind. You’re working to pay the bills, with little room for risk or creativity.

It’s the safety net that allows you to say “No” to what doesn’t align with your values and “Yes” to what does.

It’s the launchpad for building the other three Creator Capitals. It funds your education, supports your projects, and gives you the time to nurture relationships.

Many people assume they have to make millions before they can have agency. But that’s not true. What you need is enough Financial Capital to cover your life — your version of “pay for the party.”

For example, Pirate Eddie started to pay for his party from scratch in his early 20s. He had $20,000 in student loans and no savings. But he wasn’t just paying for his party. He was also paying for his parents and his future family’s parties. Pirate Eddie wanted to give his parents the lifestyle they gave up to move from Korea to the US, hoping to give their sons a better life.

At 21 years old, he landed a job in consulting making $42,000 annually. By 23, he was making 6 figures — with his compensation doubling every few years.

At 24, he bought his first house for his parents. Soon after, he bought his first-ever new car. For his parents.

At 26, he got married and at 29 he started his family of five. He had the chance to start his own business, but he couldn’t afford to take the leap into entrepreneurship because the opportunity cost was too high.

At 43, Pirate Eddie felt he had enough Financial Capital for all his parties. He quit his job, started Eddie Would Grow, and became an entrepreneur.

Could Pirate Eddie have quit sooner?

Probably. But he had a clear, predictable path to building Financial Capital that he did not want to divert from. He also knew consulting was an amazing way to build the other three capital buckets.

It was for emotional, not rational, reasons Pirate Eddie waited until 43 to leap.

He had been owned by money since the first grade, which is the earliest memory he has of realizing he was poor. He felt poorer in 7th grade when he attended an elite private school. It took decades of counseling, church, charitable giving, saving, and investing to free himself to own his money.

Which brings us to another important a-ha:

Your relationship with money is more important than your money.

And you can design your relationship with money.

When you see money as a tool (not the goal), you gain clarity, freedom, and agency. And that’s when you start living life on your terms.

Now, some of us grow up with shitty money relationships. Some of us had childhoods where the lack of money was omnipresent. Where not enough money was the thing that stopped you. “We can’t do that honey, we don’t have the money.”

When financial lack is a constant refrain, we get trained in struggle. We can be lulled into accepting lack as a “reality.”

Sadly, many people live this way.

They were never told you can design your life. They never get trained on the massive abundance in the world (created by humans who are just like you). And they never hear, “You can make abundance, too.”

We’re here to tell you: You can design your relationship with money.

There are moments in one’s life when a mental wall vaporizes and a new way of seeing the world appears.

When Pirate Christopher was 18 years old and struggling with his first startup, he did a lot of personal growth training.

The traditional school system didn’t work for him, and he understood he had to (as Chicken Soup for The Soul author Jack Canfield said) “change the tapes.” So he self-curated an education through books, tapes, and courses. But his perspective on money finally changed when he attended a seminar where workshop leader Bix Bickson interacted with a woman owned by money. Money was the excuse for every problem in her life. Lack of money controlled her. She believed she could not make money. She believed that only crooked people got rich. Struggling was part of her identity. (Just like it was part of Pirate Christopher’s — lack of money owned him, too). Whenever Bix tried to make a point, she would argue with him about money.

Finally, Bix erupted. “HEY! Listen. There is a lot of money in the world right?”

She responded, “Ya, but…”

“Would you agree there is a lot of money in the world?” Bix asked.

She kept arguing with him about how bad her life was, saying he didn’t understand.

“There is a lot of money in the world, right?” Bix kept asking.

The interaction got hot.

“YES.” she finally said. “There’s a lot of money in the world, Bix.”

To which he cheered, “GREAT! Now go out and get some!”

While Pirate Christopher watched the interaction between Bix and the woman, he agreed with the woman. In fact, he thought Bix was mean to her. But when Bix said, “Go out and get some!” he thought.

🤔 What if Bix is right?

Ten years later, Pirate Christopher was a 28-year-old millionaire running marketing for a publicly traded software company in Silicon Valley.

You can design your relationship with money.

You can be a legendary person with money.

You can make a big difference with money.

But without Financial Capital, you’re stuck trading time for money, which limits your ability to take risks or pursue meaningful work. To build it: Simplify your finances. Save consistently. Invest wisely. Avoid lifestyle inflation. Use the tools we share later on in this mini-book to understand your true needs.

Making money is a legendary thing, so let’s dig into how you get there.

How To Build Your Financial Capital

Growing your Financial Capital is possible, whether you have $10 or $10,000,000. The amount you start with matters less than having a plan and sticking to 3 key steps:

Know your expenses and keep it simple.

Invest sequentially into safe, smart, and speculative buckets.

Own your money and be free by building a financial runway.

The ultimate goal is to own your money — don’t let it own you. Financial freedom happens when you reach a point where your (after-tax) income from investments equals your yearly expenses. At that point, your money works for you.

Now, let’s break down each step.

Step 1: Know your expenses and keep it simple.

The first step is understanding your money: what’s coming in, what’s going out, and where it’s going. Most people struggle here because they don’t take the time to track their expenses, or they overcomplicate the process. Here’s how to simplify:

Sort expenses into two buckets: must-haves and nice-to-haves. Must-haves are essentials: rent, utilities, food, insurance, and debt payments. Nice-to-haves are discretionary: dining out, travel, streaming subscriptions, and upgrades to your essentials.

Review your nice-to-haves every 3 months, separating them into two categories:

Momentary joy: Expenses that bring fleeting happiness.

Lasting joy: Expenses that bring enduring satisfaction or value.

Cut the momentary joy expenses. Keep the lasting joy ones.

Look at your must-haves once a year and ask, “What must be true to cut 10% here?” If cutting 10% makes a meaningful difference in your financial runway, consider it.

For example, Pirate Eddie’s legendary 30-year-old Excel spreadsheet is his go-to tool for tracking expenses, income, and investments. It’s evolved to include scenario planning and helps him make data-driven financial decisions.

But not everyone is an Excel wizard.

After avoiding personal finance tracking for years, Pirate Katrina found a straightforward tool that worked for her, a Wealth Planner that makes it simple to track monthly expenses and see an annual review. This makes managing her finances feel less overwhelming and more empowering.

With Pirate Christopher’s dysfucklia — the medical term for “mix of several learning differences” — he learned to manage his finances by marrying well and finding a legendary accountant.

This underscores an important point.

Designing a financial system that works for you is more important than following a generic financial plan.

There’s lots of content out there on how to manage money. You should research, read, and create a version that works for you. Here are a few resources Pirate Katrina found helpful when she started building her Financial Capital a few years ago:

The key to success in this step is simplicity. If your financial plan is too complicated, you won’t follow through. Choose a system that fits your life and stick to it.

Step 2: Invest sequentially into safe, smart, and speculative buckets.

Most people live on the financial edge.

Only 28% of people have at least six months' expenses saved, and 72% are at radical financial risk.

The second step to building Financial Capital is to invest sequentially — starting with safety nets before moving on to growth and risk. This approach makes sure you’re always building on a stable foundation.

Start with Safe Investments (Your First Safety Net)

The first step in investing is to create a financial safety net. These are the resources you can access in a day, with no risk, to handle life’s inevitable right hooks.

Build a Rainy Day Fund: Save $500 in a high-interest savings account. This is your buffer for small emergencies like car repairs or unexpected bills.

Pay Off High-Interest Debt: Get rid of any debt with double-digit interest rates, such as credit cards or payday loans. Paying off a credit card with a 20% interest rate is like earning a guaranteed 20% return on your money.

Make Bulk Purchases: Buy essential items in bulk at discounts of 15% or more. This is an overlooked but effective way to earn immediate returns on your spending. You earn a 15% return right away!

Save 3-6 Months of Must-Have Expenses: Set aside three to six months’ worth of must-have expenses in a savings account. This fund is your first true safety net, giving you peace of mind if you lose income or face unexpected expenses.

Pirate Eddie’s First Safety Net

At 21 years old, Pirate Eddie had $20,000 in student loans and a few hundred in revolving credit card debt from a post-college trip to Europe with friends. But when he started his first job, he received a $2,000 signing bonus. He immediately used it to pay off his credit card debt and put $500 into a rainy-day savings account.

His must-have expenses were simple: rent and transportation. To save on rent, he shared an apartment with a college buddy who was also in consulting. They decided not to buy cars since they traveled most of the week for work, opting instead to rent cars on weekends when needed. (This was the late ’90s—long before Uber!)

Pirate Eddie kept his nice-to-have expenses at a minimum, even sleeping on a mattress without a bed frame. “Furniture is a nice-to-have,” he thought. His logic was simple: he was rarely home, spending most of his time in hotels, on planes, or at the office. When his mother visited and saw his bare apartment, she cried at his lack of furniture.

But to Pirate Eddie, that moment proved he was managing his must-haves and nice-to-haves correctly.

(And he dislikes furniture to this day.)

By keeping his expenses low, he focused his energy on building his first safety net. With his disciplined approach, Eddie quickly paid off his student loans, putting himself in a position to move to the next level of financial freedom.

Starting with the basics — rainy-day savings, minimizing debt, and simplifying expenses — creates a strong foundation for building Financial Capital.

Once your first safety net is in place, you can begin working on smart investments.

Move to Smart Investments (Your Second Safety Net)

Once your immediate safety net is in place, it’s time to take all the money beyond must-haves and nice-to-haves and invest it. This puts your money to work in smart investments (assets with moderate risk and solid growth potential) that you can access within a week.

We’re about to walk you through some very important foundational knowledge about how to get a handle on your personal financial situation.

But before we do, we want to share something super basic and super powerful that we are constantly surprised many people don’t know. (We had to be taught this too. We felt stupid we didn’t understand this too. And we’re deeply grateful to those who showed us.) So now we’re showing you.

How to turn $5,000 into $90,000 while doing nothing.

If you’re newer to personal finance, you’ll want to read this and understand it.

The S&P 500 is a basket of the largest, most valuable 500 companies on US stock markets. The average return on investment in the S&P 500 over the last 50 years is 12.393%. Investments “compound” over time. Meaning if you earn 12.393% in one year. The next year you’ll earn 12.393% on top of the 12.393% you earned last year.

So if you invested $5,000 today in the S&P 500, you’ll have approximately $89,577.50 in 25 years.

That’s how you take $5,000 and turn it into $90,000 by doing nothing.

How to turn $25,000 into $500,000 while doing nothing.

Now, just for fun, let’s see what happens to $25,000 over 25 years invested in the S&P 500.

$447,887.50 is what happens.

Yup. $25,000 today will be worth half a million dollars in 25 years.

This is the power of compounding. This is the power of passive income. You make money doing nothing. This is why the rich get richer. And this is how the poor (like the three of us) get rich.

Practically, here’s what else helps:

Employer Benefits: If your company offers a 401(k) match, contribute the minimum required to get the full match. It’s free money!

Money Market Fund: Put 10% of your investment capital into the highest-yield money market fund available at a brokerage. This ensures liquidity with better returns than a basic savings account.

Index Funds: Allocate the rest to low-cost index funds like the S&P 500 or Nasdaq QQQ through providers like Vanguard or Fidelity. These funds offer diversification, consistent growth, and low fees.

Consistency Over Timing: Invest regularly to dollar-cost average. Avoid trying to time the market. Remember, even professional money managers fail to beat the S&P 500 nine times out of ten. As Warren Buffett advises, this is the safest and smartest strategy for long-term wealth building.

The goal of smart investments is to build several years of must-have money that you can easily access. With this second safety net in place, you’re prepared for bigger opportunities or setbacks.

Advance to Speculative Investments (Your Long-Term Safety Net)

Once you have a few years of financial runway in smart investments, you can speculate.

Speculation is about calculated risks: understanding that some bets will fail, learning from those failures, and improving over time. It often has a negative reputation, but it’s not inherently good or bad. It’s all about timing and execution. Done right, speculative investments can build long-term wealth and even create a multi-generational safety net. It involves higher risks but gives you the potential for outsized rewards.

Here’s how to approach speculation wisely:

Start Small: Only invest money you’re comfortable losing. This ensures one bad bet won’t derail your financial stability.

Leverage Your Expertise: Pick one lane where you have an information advantage and stick with it. For example, Pirate Christopher invests in startups because of his deep expertise in Category Design. But Pirate Eddie focuses on public Category Queens like Tesla and real estate on the Big Island, areas where he has strong knowledge and insights. While Pirate Katrina prefers real estate in the Midwest, where she understands the local culture and economic drivers.

Avoid the Big Three Mistakes:

1. Never Speculating: Missing out on opportunities by staying overly cautious.

2. Speculating Too Early: Taking big risks without first securing safe and smart investments.

3. Speculating Blind: Investing blindly without having data flywheels or feedback loops to guide your decisions.

Create a Data Flywheel: Speculation isn’t gambling. Use tools, research, and feedback to identify patterns, refine your strategy, and make better decisions over time. Focus on markets you know well to avoid areas where you don't have the same level of confidence or knowledge.

The key to speculation is being ready. Speculating too early or with the wrong mindset can set you back years. But when approached strategically, speculation will help grow your Financial Capital and secure your future.

Just be prepared for some hard-earned lessons.

Smart and Speculative Investing (At the Right Time)

Here’s what happens when you skip steps — and how to recover from those mistakes.

Pirate Eddie lost a ton of money by prioritizing speculative investing over smart investing. At 23, fresh out of college and making six figures, Eddie took sudden jumps in income from promotions and annual bonuses to invest regularly in his 401(k) and outside accounts.

Smart Move: When Eddie’s salary allowed, he bought his first house for his parents. This fulfilled an emotional goal but came at a cost: Eddie raided his 401(k) for the down payment. While this wasn’t a traditional “smart” investment, it provided stability for his family and created Relationship Capital that paid dividends in trust and support.

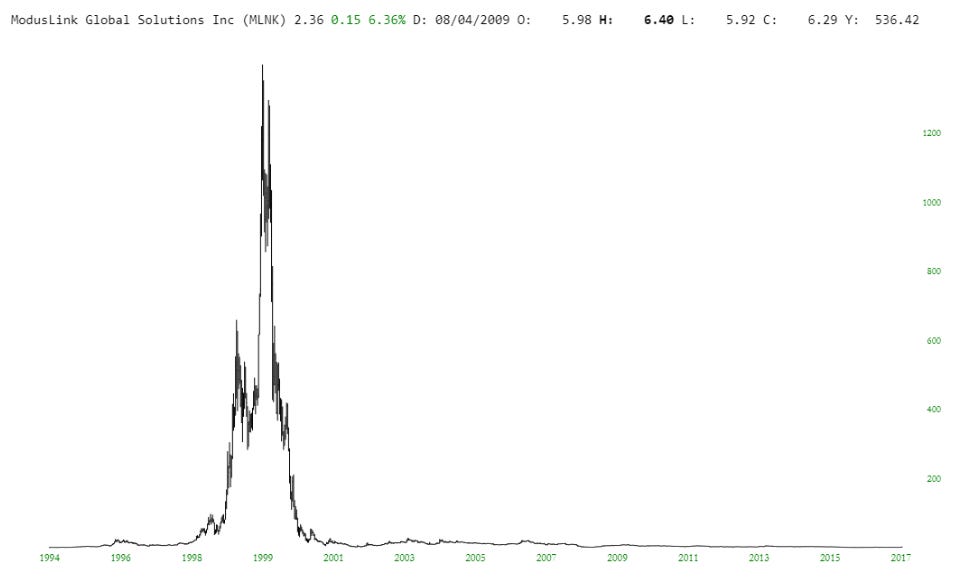

Costly Mistake: Around the same time, Eddie opened a Charles Schwab account to speculate in dot-com stocks (like 187 million other Americans at the time!). Watching colleagues rake in tens of thousands trading internet darlings like Yahoo and Broadcom, he jumped in without an information advantage. Lured by the hype, he invested in stocks like CMGI (now ModusLink) — and promptly lost a lot of money.

By 26, Eddie had learned his lesson and returned to the basics of smart investing:

Shift to Simplicity: Eddie shut down his Schwab account and moved everything into low-cost Vanguard Index Funds. Time in the market is far superior to timing the market.

Pivot Your Risk Profile: Getting married and starting a family lowered his appetite for risk. His wife was not into personal finance and disliked the complexity of multiple accounts and investments. She helped Pirate Eddie realize smart investing is not necessarily picking stocks and beating the market, but rather keeping things simple so that you’ll stick to it.

Hone Your Craft: Eddie focused on his career, which provided steady income. While many of his peers pursued MBAs, Eddie realized his time and money were better spent building Creator Capital through writing, thought leadership, and client outcomes. This not only saved him $200K in tuition but also let him buy a house for his family.

Find a Trusted Advisor: Eddie partnered with Mark Thorndyke, a highly rated financial advisor at Merrill Lynch. Although their fees were higher than Vanguard’s, the simplicity and expertise Mark offered were worth it. His wife now had one call to make if Eddie ever went overboard — financial peace of mind.

Stick to a Rhythm: As Pirate Eddie progressed, he made his annual bonuses a cornerstone of his investing strategy. Each year, he divided the money between charitable giving and investments, keeping his approach disciplined and consistent.

By 31, Pirate Eddie was ready to reenter the speculative investing world — but this time, with a strategy.

Eddie spent four years writing about Category Science and honing his POV. In 2011, he published a contrarian Harvard Business Review article, “Why I’m Happy Netflix Raised Its Prices,” after Netflix raised its prices by 60% and its stock plummeted by 80%. While Wall Street analysts and media laughed at his perspective, Eddie knew better.

On August 2, 2011, when Eddie’s first HBR article on Netflix was published, Netflix stock closed at $37.63.

By December 31, 2024, Netflix’s stock had risen to $891.32 — a 2,369 percent increase.

Although Pirate Eddie did not invest in Netflix at the time, it was the first time he realized his Creator Capital on Superconsumers, category design, and category science gave him a unique information advantage over much of Wall Street.

His speculative superpower was very specific: Identify and invest in Category Queens that meet seven conditions.

Their one-page strategy solves the entire Magic Triangle.

They stub their toe temporarily, but the core business is fine.

The new category does not fit neatly into Wall Street Analyst boxes.

There are Super-Geos that show a future-state glimpse of success, today.

Weird data shows Superconsumers doing unexpected things with their money.

The category size of prize is massively underestimated by Wall Street.

Wall Street media laughs their ass off at you while taking a massive dump on you and your POV.

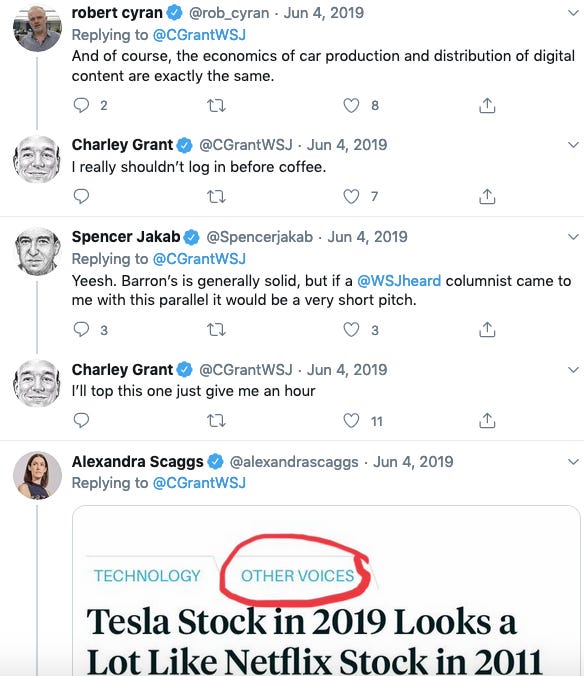

Eight years later, Eddie saw a similar opportunity with Tesla and wrote the article “Tesla Stock in 2019 Looks a Lot Like Netflix Stock in 2011” in Barron’s. Immediately after this article, several tweets emerged from the ‘experts’ like WSJ columnists, WSJ editors, and Barron’s Editors. They all mocked Pirate Eddie’s point of view.

These folks are all career commentators (e.g., journalists, analysts) who have never personally been in the arena as an executive, entrepreneur, or professional investor.

Never take advice from folks like these.

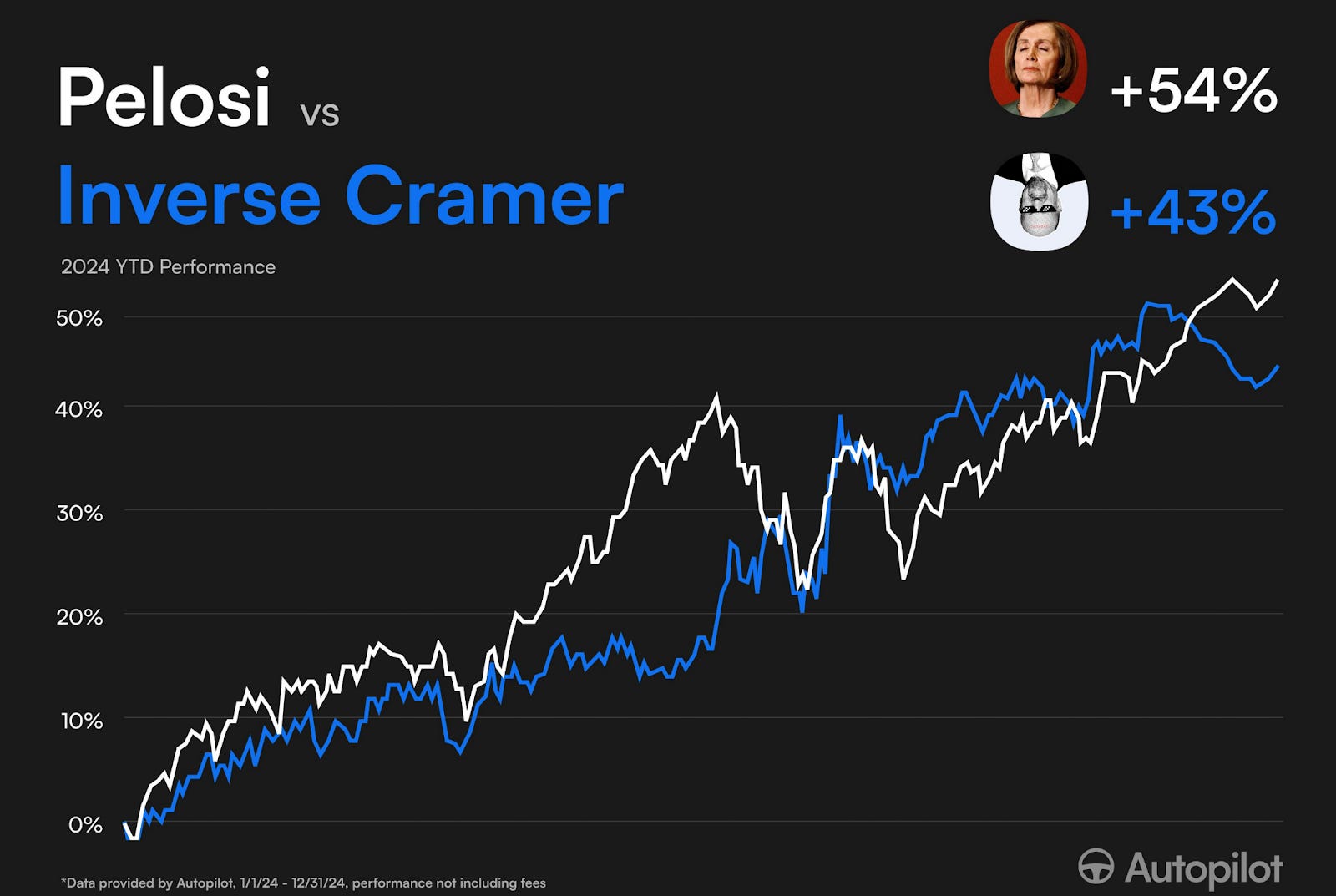

To prove our point, look at Nancy Pelosi and Jim Cramer.

Politicians like Nancy Pelosi have massive information advantages about regulations of public companies, and yet they are allowed to invest and speculate in equities. Incredibly, this is legal. Jim Cramer is perhaps the most famous Wall Street TV personality but is famous for being wrong so often that the ‘Inverse Cramer’ is a meme.

The S&P 500 went up 23% in 2024.

Nancy Pelosi and Inverse Cramer handily beat that by a wide margin.

The point: Be skeptical of any financial advice, including from us.

But especially from people who have never been in the ring!

Bolstered by the trolling by career commentators, Pirate Eddie went on CNBC Fast Money to share his POV regarding weird Superconsumers. He explained how Prius owners, the most rational and functional car buyers ever, were trading up to the Tesla Model 3.

On June 4, 2019, Tesla closed at $12.91.

On December 31, 2024, Tesla closed at $403.84 — a 3,128 percent increase.

After publishing articles and appearing on CNBC, Eddie invested personally in Tesla. He turned a five-figure investment into a six-figure return. And as his conviction grew, a seven-figure one.

(Note: This is not investment advice!)

Pirate Eddie spends many hours per week consuming content about Tesla, doing category science, and asking himself if he should add/hold/pare back his position. As of now, he is converting all his charitable giving into a donor-advised fund, which should allow him to donate 1% of his TSLA holdings each year without paying huge capital gains tax. It frees up a significant amount of cash flow without paying a massive tax bill.

Speculation is risky, and even Eddie has made costly mistakes.

Fraud Loss: A six-figure private credit investment taught Eddie the importance of due diligence.

Angel Investing: After failing in 9 out of 10 angel investments, Eddie realized his strengths were in public markets where he had a clear edge and a massive, and legal, information advantage.

As Andrew Carnegie said, “Put your eggs in one basket and watch that basket.”

Just make sure your safe and smart investments are in place before you do this with your speculative investments.

By following these steps — starting safe, building smart, and advancing to speculation — you create a balanced, resilient investment strategy. No matter what happens, you’re protected, prepared, and positioned to grow.

Step 3: Own your money and be free by building a financial runway.

Many people go through life being owned by money. As a result, they are never free — and it is as ironic as it sounds.

It doesn’t matter how much money you have (or don’t have).

If your money owns you, your money owns you.

Legendary Japanese self-help author Ken Honda has sold over 8 millions books. On the press tour for his book “Happy Money” he did a podcast with Pirate Christopher. He offers up a lighter, more fun lens on money. He says he loves paying his taxes because paying taxes means he made money. And the taxes help pay for great things. Honda can sound a little woo-woo for some, but his playfulness about money is undeniably refreshing.

According to Honda, “Happy Money” is money connected to joy:

It creates positive energy and makes people smile.

It acts as a form of love, given and received with gratitude.

It carries intention, shaped by the emotions and energy behind every transaction.

He says the energy and emotion associated with financial transactions determine whether money is "happy" or "unhappy." He encourages us to cultivate a mindset of gratitude and appreciation when dealing with money, even saying "arigato" (thank you) when you spend money. That’s a legendary (different) way to think about owning your money.

But here’s the real a-ha:

The goal of a financial runway isn’t retirement. It’s not about quitting work forever. That’s one of the biggest lies society tells us.

The Big Retirement Lie & The Truth About Work

Traditional retirement — the dream of grinding for 40 years to save enough money to not work for 20 or 30 years — doesn’t add up. Economically, socially, or emotionally. It’s a fast track to accelerating social isolation and senility.

Underlying The Big Retirement Lie is a second lie: Work is bad.

As humans, we are wired to work. Work is legendary! But work can be corrupted by bad systems, toxic cultures, and a lack of alignment with our different superpowers. (Think: Steph Curry in a dunk contest…not so much). True work, the kind that aligns with your unique abilities and brings purpose to your life, is heaven. (Think: Steph Curry hitting four 3-pointers in the last two minutes against France in Paris for the Olympic Gold medal.)

Freedom is not defined as not having to work.

Freedom is not a life without constraints, rules, or boundaries.

Constraints are not necessarily bad, and unlimited freedom is not necessarily good. Having nothing or no one tell you “no” often leads you to make stupid decisions that can ultimately imprison you. (We’re lucky to have spouses, friends, and partners who tell us no and keep us in check!) Instead, freedom is about being in the right situation — and embracing both constraints and purpose — that allows you to utilize your superpower to its fullest potential and create the greatest joy, impact, and abundance.

Think about this:

A sportscar is most free on the Autobahn, where it can unleash its power.

A dolphin is most free in the ocean, zipping through waves, and drafting behind boats.

But imagine if a sportscar and dolphin wanted to swap places in the name of freedom. Ridiculous! Freedom that contradicts design and purpose is pointless.

True freedom is getting paid to create.

Humans crave purpose.

We are designed to do extraordinary things. But those things are not always obvious — they require discovery, effort, and courage. So you have to figure out your superpower, use it to drive outcomes, and get paid handsomely for it!

Our goal for you is simple:

Find your superpower as soon as possible.

Make as big a difference to others as possible.

Get paid to create as a Creator Capitalist now — and until the day you die.

You can design a life where your financial choices fuel your freedom instead of truncating it.

A financial runway is a launchpad for something greater — a life where your work, purpose, and financial choices align.

Consider this:

The average net worth of Americans is $1.06 million, according to the Federal Reserve’s 2023 Survey of Consumer Finances. Meanwhile, the median net worth is much lower at $192,900.

In 2022, 20% of families owned a privately held business, the highest level on record.

Business ownership is a key driver of wealth.

(You want to own things that work for you, not work for things that own you.)

According to the Federal Reserve Changes in US Family Finances 2019-2022 report, families that own businesses are wealthier than those who don’t:

The mean net worth of families without a business was about $570,000.

Families that owned businesses with 2–5 employees had an average nonbusiness net worth of $1.6 million.

Families owning businesses with more than 5 employees saw their mean net worth rise to $4.1 million.

Your financial runway is more than just a safety net. It’s your launchpad for opportunity. When you pair financial independence with business ownership or other creator / entrepreneurial pursuits, you unlock a powerful combination that sets you apart. You stop reacting to every opportunity (threat) that comes your way and start creating new and different opportunities you actually want to pursue.

Yes, building Financial Capital takes time.

But so does anything worth having. Just remember the three steps:

Keep it simple.

Manage your emotions.

Own your money — don’t let it own you.

Start where you are. Track your expenses. Learn how to invest. Use the tools we shared. (It’s not hard. It’s just work.)

Financial Capital is the foundation of your runway, but it’s just one part of becoming a Creator Capitalist.

You must also build the other three Creator Capitals to create a life of radical agency.

This requires you to think about what makes you stand out.

So, ask yourself:

How do I build a reputation and use it to open doors, build trust, and create opportunities?

We’ll save that for the next mini-book.

Arrrrrr,

Category Pirates 🏴☠️

P.S. - Check out the other Creator Capital mini-books.

Reputation Capital: How The Currency Of Differentiation Creates Lifelong Opportunity

Relationship Capital: The 8 Connections That Help You Create A Legendary Career

Intellectual Capital: 5 Ways To Turn Your Knowledge Into Content That Makes Money While You Sleep

P.P.S - Know someone ready to build Financial Capital? Share the wealth.

If you know someone ready to take control of their career but needs a roadmap, share this mini-book with them.

This is just one part of our upcoming course and book, Creator Capitalist, where we’ll dive even deeper into designing your career, building your capitals, and getting paid to be you. We’ll share more as we build it out!

So, pass it on — and let’s start a conversation about building a future on your terms.

This was a monster F*cking newsletter. Thank you!!!!

This one👇 is 🔥

"When your life is about living (and money is simply the tool to fuel it), you can have radical agency."

Agency, authenticity, autonomy (author) - all running in similar circles of meaning. 🙌